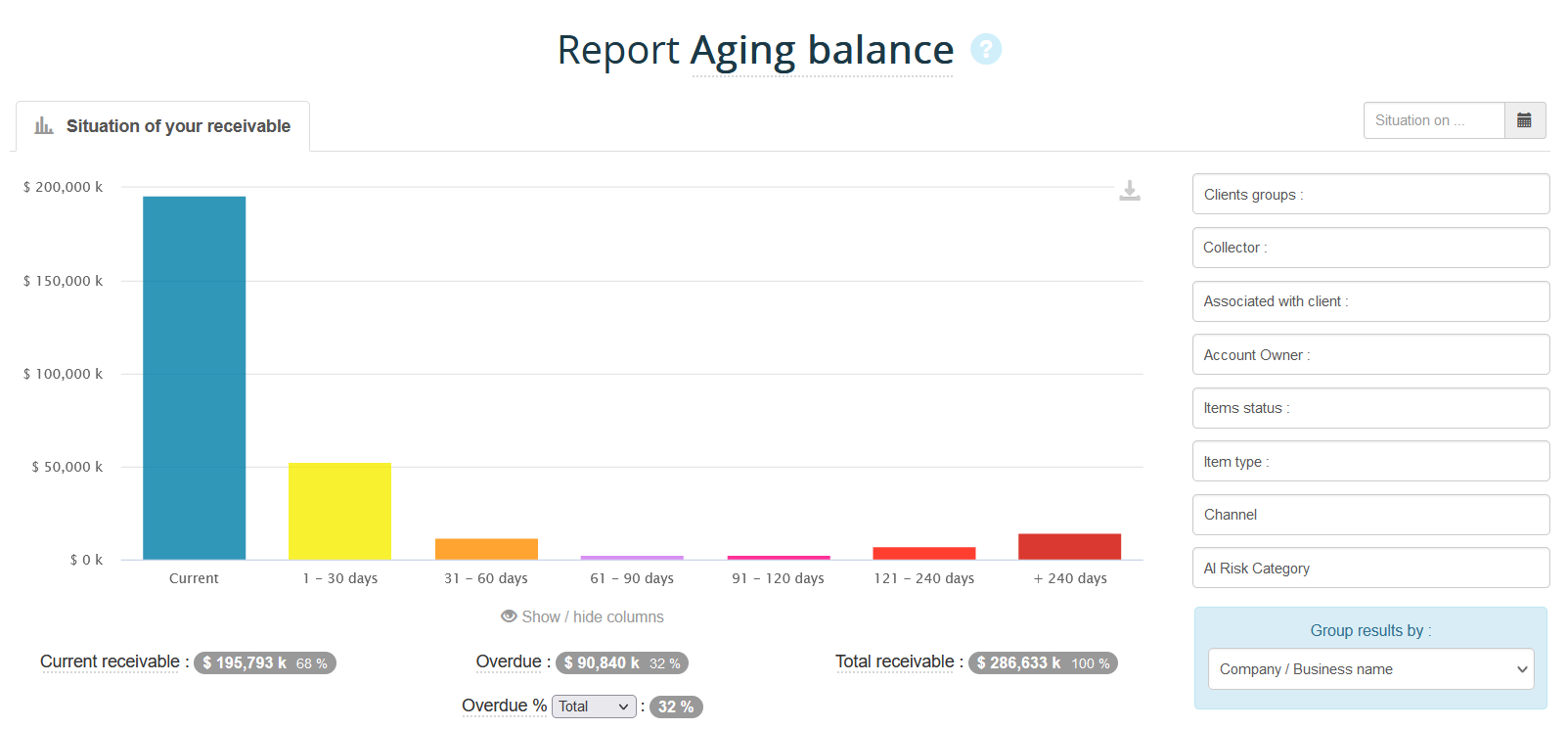

Accounts receivable represents the sum of trade receivables (invoices, credit notes, unallocated payments, etc.) that are open in accounting, i.e. not yet paid and cleared.

It appears on the assets side of companies' balance sheets in the current asset category. This terminology illustrates the temporary nature of a receivable, which is supposed to be 'actual' and 'current' and be settled within a relatively short period of time after it is issued.

What are the risks associated with customer outstandings?

Outstanding accounts receivable tie up the company's financial resources because it corresponds to a sum of money that is "out", and which is potentially at risk since the payment of invoices is not certain. In addition, this amount depreciates over time without compensation, particularly during periods of high inflation.

It is therefore in every company's best interest to reduce this outstanding amount, as it represents:

- A risk of non-payment and therefore losses that wil impact the income statement and equity.

- A burden on the company's cash flow and its investment and development capacity.

- A risk of depreciation due to inflation

Outstanding receivables: A critical requirement

Accounts receivable are therefore an important contributor to working captial requirements.

However, it is necessary since the granting of a payment time in commercial relations between experts is frequently unavoidable. It should be noted that payment terms are governed by the law in some countries, and have a time restriction. As example, since the introduction of the NRE law in Europe, the maximum payment period is limited to sixty days or forty-five days at the end of the mounth (depends on the country). It should be noted that the Law also allows for late payment penalties or default interest to be applied in the event of late payment.

How to manage your outstanding accounts receivable?

As a result, companies bear a portion of outstanding accounts receivable and must manage them in various ways.

Customer risk management in order to identify and reduce the risk of non-payment

There are many techniques and tolls that can be used to carry out credit analyses and covering overdue loans. The first step to reintegrate payment terms into the commercial negociation in order, for example, to get advance payments at the time of the order and to shorten the payment term granted. Secondly, some companies, credit insurers and banks can guarantee the payment of the bills. Check out our Risk Management tutorials to learn more about this topic.

Rapid identification and resolution of disputes

Sometimes, your customer had a good reason not to pay: an administrative problem, a quality problem or a delivery problem, etc. A preventive follow-up, carried out before the deadline, allows you to be aware of the problem as soon as possible in order to solve it as quickly as possible and to get paid while preserving customer satisfaction.

Implementation of an efficient collection of issued invoices

The application of systematic dunning scenarios and daily monitoring of exchanges with accounts payable gives credibility to your company in terms of the quality of its management and makes it possible to speed up collections and reduce the DSO.

Digitalization of customer relations.

The three points of attention and management mentioned above are part of the digital revolution in customer relations that has been underway for several years. Portals, interconnections between systems, fluidity of access to information for all those involved in the commercial relationship, automation or semi-automation of dunning actions, etc. Digitisation is making it possible to increase the efficiency and fluidity of inter-company exchanges. The implementation of digital solutions is also essential, especially with the advent of electronic invoicing. Companies that have not anticipated or at least jumped on the bandwagon will find themselves disconnected, in every sense of the word. They will have to compensate for the automated and instantaneous work of digital tools with manual tasks. The digitalization of the commercial relationship in tis financial aspects makes it possible to do ten times more and ten times better in ten times less time!

The challenge of outstanding receivables in the digital age

With the outstanding number of customers, many challendes are at stake for the company, wether they are of a financial or quality nature. By developing what appears at first glance to be a simple asset item on the balance sheet, we find everything that makes the strength and sustainability of a company: its financial balance and cash flow, the quality of its sales process and its products and services, its management and its modernity in the integration of digital technologies. Digitization does not mean dehumanization; quite the opposite. It is by removing from humans the dauntung tasks for which they are infinitely less efficient and relevant than interconnected digital tools that they can devote their time and their incomparable added value to the essensial part of the commercial relationship: human relations and the resolution of complex problems requiring many forms of intelligence (emtional, antivisual, anti-existent, intuitive, etc.), which the machine is far from acquiring.